Pour la version française, cliquez ici.

Click here to download as a .pdf document

Pieridae has been working on an LNG terminal at Goldboro, Nova Scotia, for some years now. The terminal could be considered well on its way, as a construction permit has been granted. Major German utility company Uniper signed a take-or-pay agreement for all the gas from the terminal’s first train. This agreement includes a US $4.5 billion loan guarantee from the German government through the KfW investment bank: US $3 billion for the construction of the terminal, and US $1.5 billion for the development of upstream assets.

All is under one condition: the gas developed with German funding must not be fracked.

To some extent, Germany forbids fracking on its territory and doesn’t want to be caught subcontracting this unclean process to outside jurisdictions. Do the company’s assets allow it to only provide conventional gas to its German customer, or will it eventually rely on fracked gas during its twenty years contract with Uniper? To answer this question, we need to look at Pieridae’s potential prospects for sourcing natural gas. The following map (Exhibit 1), which Pieridae presented on numerous occasions as its plan to source and transport gas, offers many answers. During its latest corporate presentation, the company explained it will feed Train 1 with gas from its assets in Alberta, following deals with Ikkuma and Shell. Meanwhile, Train 2 would rely on gas from New Brunswick and the eastern part of Quebec. We will also examine the case of the Sable offshore field in Nova Scotia as well as Utica and Marcellus shale in the U.S.

As we go, it will become clear that:

1-the majority of the gas fed to Germany within Pieridae’s project would be fracked gas;

2- Germany’s subsidy to Pieridae might increase hydraulic fracturing extraction in areas that weren’t affected much by the process so far.

Exhibit 1

Conventional natural gas opportunities in Western Canada

Ikkuma’s assets in the Alberta foothills

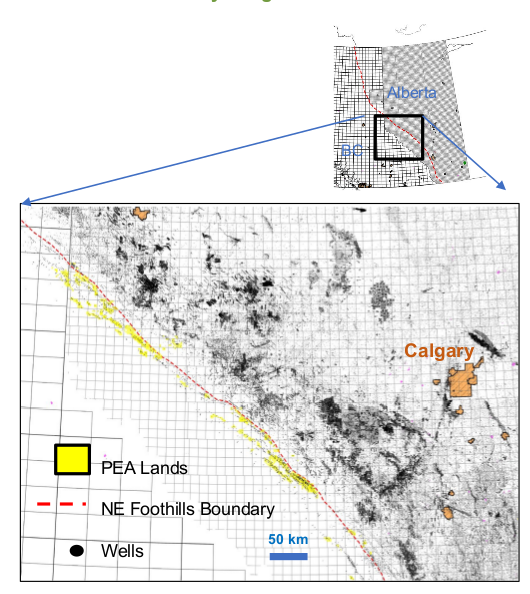

In August 2018, Pieridae announced a merger with Ikkuma. Below is a map of Ikkuma’s assets (shown in yellow on the map, Exhibit 2), from its latest presentation to shareholders. (Shell’s assets are located roughly in the same area, west of Calgary.)

Exhibit 2

Upon sale, Ikkuma separated its assets into oil and gas producing wells. Pieridae acquired only the gas producing wells. The Ikkuma wells yielded an average of 101 MMcf/d in Q3 2018, and the production rate may increase in the future. However, unless Pieridae discovers more conventional resources in the area, they will not be able to maintain this extraction rate for more than 18 years, as the fields hold resources and reserves of only 670.5 bcf.

Pieridae’s acquisition of Shell assets

The deal Pieridae concluded with Shell involves three sour gas processing plants, where sulfur will be removed from the gas : Jumping Pound, Caroline and Waterton. The Jumping Pound facility isn’t merely old, it is the oldest gas plant in Alberta. The Petroleum History Society published an article about it in 2002. Hence, it is very unlikely Pieridae will be able to even double the field’s current production levels.

In 2019, Shell’s upstream assets delivered 119 MMcf/d of conventional sour natural gas. By the end of 2019, Pieridae’s upstream production reached 243 MMcf/d. After the transaction with Shell, Pieridae’s total reserves amounted to 1,078 bcf according to an audit published in the Annual Information Form published April 15, 2020 (Exhibit 3):

Exhibit 3

With constant extraction from this 1,078 bcf net reserve over 20 years, Pieridae would obtain 54 bcf of conventional gas per year, which equals 147 MMcf/d. In other words, those assets are probably nearing or even past peak production. 147 MMcf/d makes up less than a fifth of the required gas to feed Train 1. If Pieridae extracts 243 MMcf/d continuously, which is impossible given the necessary decline in production, it would dry up its reserves in less than 14 years. To add to the problem, they would not even produce a third of the gas required for Train 1.

The numbers are consistent with Pieridae’s business model, which relies on outsourcing at least 50% of its gas, as outlined in a Laurentian bank document: « To supply both LNG Trains will require up to 1.5 bcf/d of raw gas, and Pieridae will likely seek to own up to 50% of that requirement, and source the remainder through the North American gas grid. Our section on Transportation [Exhibit 1] identifies the pipeline routes available to the Goldboro facility. »

So far, Pieridae managed to acquire only 1,078 bcf of conventional natural gas reserves. It is highly unlikely they will be able to feed Train 1 entirely with conventional gas from Alberta, since the entire Western Canada conventional gas supply is slowly drying up as well.

Conventional production declines in Alberta and British Columbia

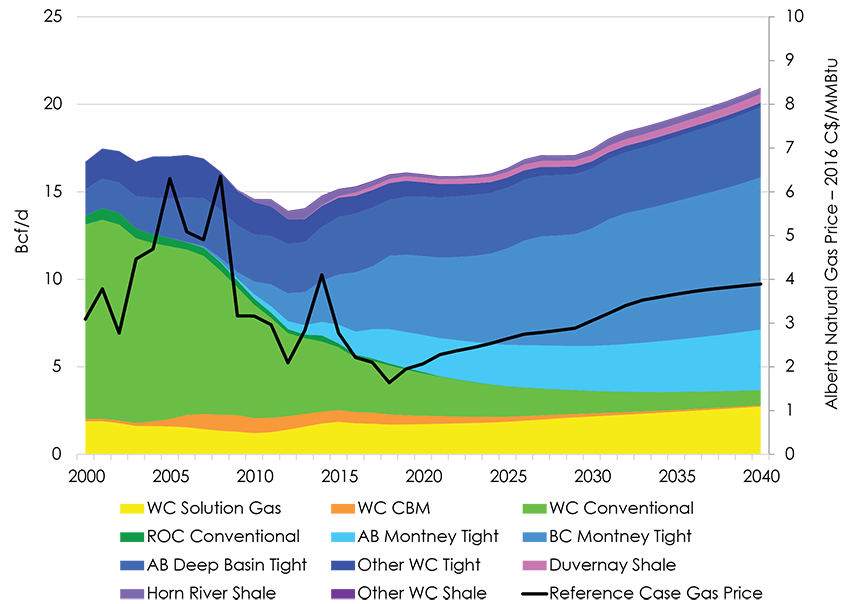

The light green portion of the graph (Exhibit 4) represents conventional natural gas production in Western Canada from 2000 to 2040, with a clear trend towards exhaustion.

Exhibit 4: Natural gas production by type and price forecasts

Source: National Energy Board of Canada

In its Canada’s Energy Future 2018 Supplement, the National Energy Board of Canada states: “Western Canada conventional gas is projected to decrease from 2.96 bcf/d in 2017 to 0.87 bcf/d in 2040.” This decline rate is more than threefold. If it is applied to Pieridae’s assets, we could forecast its conventional gas production would decrease from 243 MMcf/d to 71 MMcf/d, with an average of 157 MMcf/d. These estimations are very close to what Pieridae holds as reserves, spread over the same time span.

Western Canada Solution Gas (shown in yellow) “is gas produced from oil wells in conjunction with the crude oil.” Heavy oil does not contain any natural gas or lighter solvent, hence the term “heavy”. Solution gas comes from light oil. A large amount of light oil currently extracted in Western Canada comes from fracking, and the only way to increase solution gas supply is to exploit more fracked oil in Western Canada. This scenario would not allow Pieridae to sell it to Germany as conventional gas.

Pieridae already processing fracked gas at not-yet-acquired Caroline plant

The deal between Pieridae and Shell involves the transfer of three gas processing plants, including a more recent facility, the Caroline plant. In its latest annual financial statement, Pieridae declares the following: “The Company also generates gas processing revenue of $6.8 million (December 31, 2018 $0) for fees charged to third parties for processing through facilities in which Pieridae has an ownership interest.” The facility is most likely processing gas for Shell as part of the deal to acquire its acid gas assets. The article Sweet future for Shell’s Caroline Plant confirms the Caroline field is nearing 95% recovery and that Shell wanted to convert the Caroline plant to process gas from the Rocky Mountain House play. On its corporate website, Shell states it “has been pursuing the production of light tight oil, gas and liquids from the Duvernay play, in this area.” Duvernay is a tight play known to require fracking for oil and gas extraction.

Consequently, Pieridae will have the opportunity to buy fracked gas already processed at the Caroline plant. If Pieridae lacks the reserves to feed its first train with conventional gas only, will it buy the gas from its partner Shell? Or will it find another partner who could provide more expensive, but already treated fracked gas? Alfred Sorensen partially answers this question in the April 16, 2020 corporate presentation: “The most significant asset we acquired was three deep cut plants: the Jumping pound, Caroline and Waterton. Between the three of them, they represent about 750 million a day of processing capability, and that number is a big part of how we’re going to supply our first train. One train requires about 800 MMcf/d, so you can see the two numbers are very close in relationship. […] That’s how […] we will begin to service our first train.” In the same presentation, we learn that Pieridae produces 204 MMcf/d, but processes 420 MMcf/d of gas at the three plants it will soon own. The difference is most likely fracked gas.

Pieridae has a deal with Shell to process its gas from the Rocky Mountain House play. They want to use all the processed gas at the three plants to feed the first train of the terminal, which will supply Uniper.

One way or the other, it appears impossible for Pieridae to feed its first train entirely with conventional gas from Western Canada. Nowhere will they find the 800 MMcf/d of conventional natural gas required to feed the terminal’s first train over the next twenty years.

Could Pieridae rely on assets in Eastern Canada and the U.S. to find the missing part of its conventional natural gas?

Conventional gas in Eastern Canada?

Pieridae uses the map (Exhibit 1) during many corporate presentations to indicate where it will source its gas from and how it will be transported all the way to its terminal. Let’s look at these sources, beginning at the furthest east gas deposit.

Nova Scotia’s Sable field : gone!

“The third option for Pieridae is to source gas from offshore Nova Scotia. While the existing Sable Island and Deep Panuke gas fields are being decommissioned, the existing 300 MMcf/d production platform and Sable pipeline direct to Goldboro provide significant advantages.” (Excerpt from “On Track to Become Canada’s First Major LNG Exporter”, January 2018) In a January 3, 2019 press release, the Nova Scotia government stated: “A few days ago, one chapter of Nova Scotia’s offshore story came to an end when the Sable Offshore Energy Project delivered the last of its gas to our province.” This apparent source of gas for Pieridae’s executive is in fact so depleted that Nova Scotia’s government says it “delivered the last of its gas.”

New Brunswick : A moratorium on fracking after traumatic events

In 2014, New Brunswick introduced a moratorium on hydraulic fracturing. Before this historic moment, dozens of groups from across the province united against the industry. One of them, the New Brunswick Anti-Shale Gas Alliance, went on to sue the province. After the pro-shale Conservatives’ electoral loss and the subsequent implementation of the moratorium, the lawsuit was dropped. However, the Alliance remains active and diligent: it has stated it will go back to court if any exemption is approved.

In the years prior to the moratorium, Indigenous opposition escalated from demonstrations to civil disobedience, culminating with a militarized RCMP raid on a protest encampment. Arrests were made, and police cars were burned (Exhibit 5) – a traumatic incident that still affects Indigenous and police relationships six years later. An investigation of the RCMP’s misconduct has been completed, but not yet released.

Exhibit 5

The moratorium targets hydraulic fracturing, not drilling for gas. Since all New Brunswick gas reserves require fracking, no drilling is conducted in the province. And those reserves include Pieridae’s gas leases.

Five conditions must be met to lift the moratorium: a social license, a regulatory regime able to enforce health and environment protection laws, a plan to mitigate impacts on public infrastructure and manage wastewater, meaningful consultations with First Nations, and a royalty structure benefitting New Brunswick residents.

Pieridae threatens the New-Brunswick moratorium on fracking

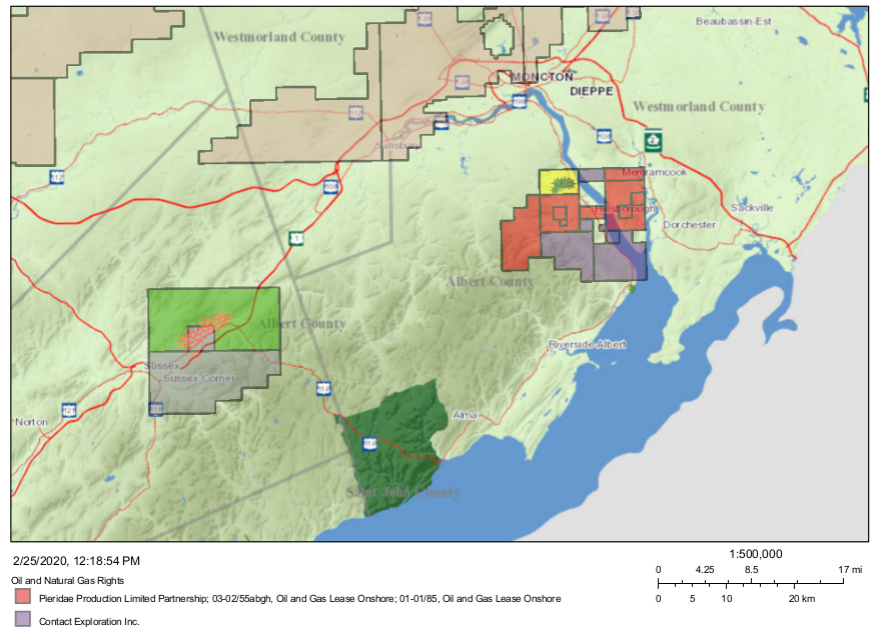

Pieridae has corporate interests in New-Brunswick assets (Exhibit 6) that could easily be connected to the Maritimes and Northeast pipeline (M&NE, dark blue line in Exhibit 1). During its presentation to shareholders in June 2018, Pieridae stated that “if Conservatives are elected, they have indicated they will lift the fracking moratorium.”

A year after their election, the Conservatives attempted a partial exemption to the moratorium in the Sussex area, where mayor Marc Thorne wishes the industry would resume its activities.

Exhibit 6: Map of gas leases in southern New-Brunswick

Source: Corporate presentation, June 2018

The McCully Field, currently the only area being considered for moratorium exemption, is represented in the lower left corner of the map (Exhibit 6) as two plots shaded in light green and gray, around the towns of Sussex and Sussex Corner. As the legend shows, Pieridae leases—in red—lay far to the east.

In the areas around Pieridae’s leases, citizens strongly oppose the shale gas industry. In fact, multiple municipalities such as Hillsborough, Memramcook and Alma have passed local ordinances against shale gas, and the provincial government gave its word to comply. The major city of Moncton, which gets its water from the leased area, has also passed an ordinance against the shale gas industry. Opposition is strong among the Wolastoq and Mi’kmaq Indigenous peoples in the province.

For now, the demand for gas in New Brunswick is low. Provincial needs are met by neighbouring fracked gas fields in the Northeastern United States. A new LNG export terminal in the province next door would increase pressure to lift the fracking moratorium in New Brunswick, against the will of the local Indigenous people and population. Pieridae might not use the German loan to directly develop its claims in New Brunswick; however, the company most likely has the will to exploit these claims once Train 2 is completed. The Goldboro LNG project and Pieridae’s plans will create a push to lift the moratorium as soon as it’s time to start drilling the area. The situation seems similar in the neighboring province of Quebec.

Pieridae’s assets in Quebec : small unconventional reserves

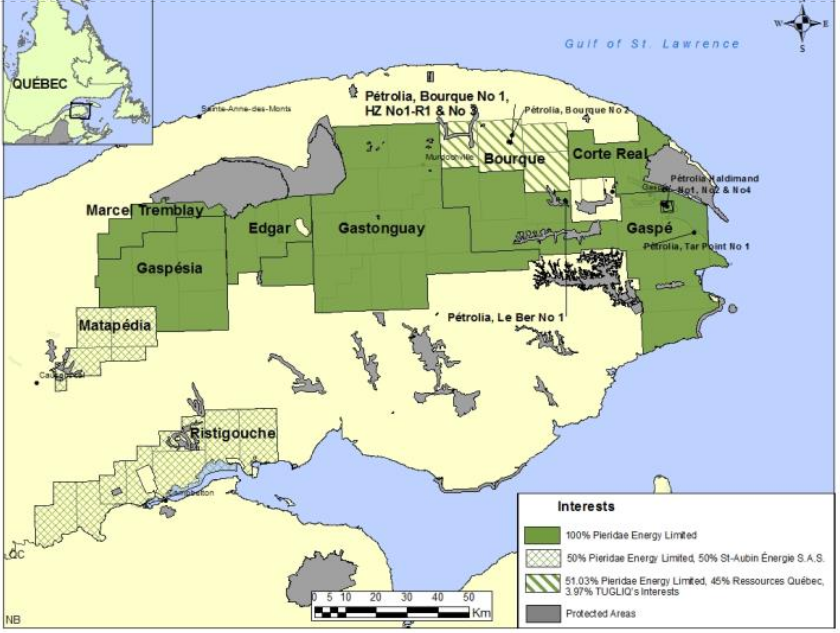

The Quebec connector pipeline (Exhibit 1) does not yet exist, since the resources are still untouched. The pipeline would connect the Gaspé peninsula (see map in Exhibit 7) to the existing M&NE Canada system. Pieridae abandoned most of the fields shown on the map in 2019 and only owns the Matapedia, Bourque and Gaspé fields at this time.

Exhibit 7: Pieridae claim in the Gaspé peninsula

Source: 2018 Presentation to shareholders

Pieridae owns three wells in the Bourque area. In a presentation to shareholders from June 2018, the company outlines that “initial production from Quebec resources will come from the Bourque field in the Gaspé peninsula” and that “permitting work for fracking [is] to be done in 2019.” The 144 bcf of prospective natural gas resources in the Bourque field (see the Sproule report, Table 6) would only provide around 1 to 3% of the gas needed for both Goldboro terminal trains over the 20-year contract with Uniper. According to the report: “The Forillon Reservoir is estimated to be in the 0.01-0.02 mD permeability range. Analogous reservoirs of this permeability range have been successfully developed using HMSF [Hydraulic Multi-Stage Fracturing] technology, however, most of these analogous reservoirs are in tight sandstone and shale reservoirs.”

No well has been drilled in the Matapedia field. Furthermore, two of the three existing Haldimand wells will need to be closed due to a Quebec regulation that prohibits exploration closer than a kilometer from residential areas.

All the gas Pieridae could send the Goldboro terminal from the Gaspé peninsula would be fracked gas. Unfortunately for the company, social licences for fracking in Quebec do not exist. After a year-long protest camp blocking the Galt project (which belongs to another company and is close to being developed), a survey was conducted in the fall of 2017. This survey revealed only 25.6% of the local population supported the Bourque project if fracking was needed. The surveyor did not mention the company’s independent report, according to which the Bourque site cannot be developed without fracking. Closer to home, in Haldimand, only 12.4% of the local population supports oil and gas development if fracking is required, which is the case. The majority of residents (49.3%) would oppose Pieridae’s project even if no fracking were done.

Exhibit 8: Support of Pieridae development projects in the Gaspé peninsula

Source: Segma Research survey

Pieridae’s intent to feed its terminal with gas from the Gaspe peninsula would put pressure to develop an area barely touched by fracking.

Marcellus and Utica regions : Mostly fracked gas

In 2014, conventional extraction of fossil gas in the Marcellus region declined to 5% of the total extraction volume, i.e. about 750 MMcf/d for the whole play. In the Utica region, conventional fossil gas production gravitated around 180 MMcf/d for over 5 years before the shale boom in 2012 and 2013.

Exhibit 9: Utica region natural gas production

Source : U.S. Energy Information Administration

Unless Pieridae signs agreements to buy conventional gas from the Utica and Marcellus plays, 85% to 95% of its purchases will consist of fracked gas. This proportion is very likely to increase in the next 20 years, as the conventional supply will eventually dry out. A long-term agreement is just speculation, since Pieridae only plans to use gas resources south of the U.S. border as a backup if Eastern and Western Canada reserves are not enough to feed its terminal.

Germany’s KfW loan guarantee : Lack of conventional reserves and pressure to develop fracked gas in Eastern Canada

Here are the words of Stéphanie Fortin, spokesperson for GNL Québec, a similar sized LNG project in Saguenay, Quebec : « Nous avons toujours été clairs et transparents concernant la provenance et la méthode d’extraction du gaz naturel qui serait utilisé dans le cadre de notre projet ; 85 % de notre approvisionnement sera effectivement extrait selon la méthode de fracturation hydraulique. » (“We have always been transparent on how we will source and extract the natural gas used for our project; 85% of our supply will actually be extracted through hydraulic fracturing.”) GNL Québec and Goldboro are similar projects with similar sources, except that GNL Québec does not hold a permit to import U.S. gas and then export it. Therefore, it cannot rely on fracked gas from Utica or Marcellus shale south of the U.S. border. GNL Québec also will not tap into Quebec or New-Brunswick’s risky fracked gas assets. All the gas would come from Western Canada, and the company’s spokesperson clearly states the mix contains no more than 15% conventional gas. In the future, this proportion will only decline.

Despite Pieridae’s efforts to produce its own gas and buy upstream assets, it must face the reality that conventional fields are depleted. The company must admit it cannot provide 800 MMcf/d of conventional gas to the Goldboro terminal, even if this means losing the US $4.5 billion loan guarantee from KfW to build the first train and expand upstream assets.

Does Pieridae know about the current decline in conventional gas production and resulting price hikes? When they applied for a licence to import and export before the National Energy Board of Canada, they produced a study by Ziff Energy, a division of Solomon Associates. Here is what Ziff Energy had to say about conventional gas in North America:

6.2.2.4 Conventional Gas

Gas from reservoirs with greater permeability has been developed since the late 19th century. Most conventional-gas plays are mature, higher cost, and have passed their peak production. Reserves per well are small, resulting in high costs. Before the advent of shale gas, a record level of drilling activity was required to maintain gas production levels in North America. Aggregate gas production has been in decline for more than a decade. For example, the US Gulf of Mexico region, the former workhorse of North American gas production, is declining mainly due to the sharp fall in gas production on the shallow-water Gulf of Mexico shelf. Some old, mature plays are experiencing a new lease on life as producers apply new and evolving technologies, sometimes with spectacular results, such as the Granite Wash in the US Anadarko basin. Ziff Energy assumes the production declines will continue, though at a moderated pace as improved technologies (horizontal wells, multistage fractures) enhance play economics.

This explanation comes from Pieridae’s own expert report. Of course, the US $4.5 billion loan guarantee from the German government is a good enough reason to lie about the acquisition of Ikkuma and Shell’s “conventional” assets. The Goldboro LNG terminal would not only rely on tight and shale gas supply, but also also increase the demand for fracked gas in Eastern Canada. This would put pressure to lift the ban on fracking in New Brunswick and push against social license requirements, as well as a partial ban, in Quebec. For this reason, Germany must not commit to a loan guarantee for the Goldboro LNG terminal project.

Pieridae has been working on an LNG terminal at Goldboro, Nova Scotia, for some years now. The terminal could be considered well on its way, as a construction permit has been granted. Major German utility company Uniper signed a take-or-pay agreement for all the gas from the terminal’s first train. This agreement includes a US $4.5 billion loan guarantee from the German government through the KfW investment bank: US $3 billion for the construction of the terminal, and US $1.5 billion for the development of upstream assets.

All is under one condition: the gas fed to Germany must not be fracked.

To some extent, Germany forbids fracking on its territory and doesn’t want to be caught subcontracting this unclean process to outside jurisdictions. Pieridae swore to provide only conventional gas to Germany, but is this possible? Do the company’s assets allow it to uphold this promise, or will it eventually rely on fracked gas during its twenty years contract with Uniper? To answer this question, we need to look at Pieridae’s potential prospects for sourcing natural gas. The following map (Exhibit 1), which Pieridae presented on numerous occasions as its plan to source and transport gas, offers many answers. During its latest corporate presentation, the company explained it will feed Train 1 with gas from its assets in Alberta, following deals with Ikkuma and Shell. Meanwhile, Train 2 would rely on gas from New Brunswick and the eastern part of Quebec. We will also examine the case of the Sable offshore field in Nova Scotia as well as Utica and Marcellus shale in the U.S.

As we go, it will become clear that:

1-the majority of the gas fed to Germany within Pieridae’s project would be fracked gas;

2- Germany’s subsidy to Pieridae might increase hydraulic fracturing extraction in areas that weren’t affected much by the process so far.

Conventional natural gas opportunities in Western Canada

Ikkuma’s assets in the Alberta foothills

In August 2018, Pieridae announced a merger with Ikkuma. Below is a map of Ikkuma’s assets (shown in yellow on the map, Exhibit 2), from its latest presentation to shareholders. (Shell’s assets are located roughly in the same area, west of Calgary.)

Upon sale, Ikkuma separated its assets into oil and gas producing wells. Pieridae acquired only the gas producing wells. The Ikkuma wells yielded an average of 101 MMcf/d in Q3 2018, and the production rate may increase in the future. However, unless Pieridae discovers more conventional resources in the area, they will not be able to maintain this extraction rate for more than 18 years, as the fields hold resources and reserves of only 670.5 bcf.

Pieridae’s acquisition of Shell assets

The deal Pieridae concluded with Shell involves three sour gas processing plants, where sulfur will be removed from the gas : Jumping Pound, Caroline and Waterton. The Jumping Pound facility isn’t merely old, it is the oldest gas plant in Alberta. The Petroleum History Society published an article about it in 2002. Hence, it is very unlikely Pieridae will be able to even double the field’s current production levels.

In 2019, Shell’s upstream assets delivered 119 MMcf/d of conventional sour natural gas. By the end of 2019, Pieridae’s upstream production reached 243 MMcf/d. After the transaction with Shell, Pieridae’s total reserves amounted to 1,078 bcf according to an audit published in the Annual Information Form, April 15, 2020 (Exhibit 3):

With constant extraction from this 1,078 bcf net reserve over 20 years, Pieridae would obtain 54 bcf of conventional gas per year, which equals 147 MMcf/d. In other words, those assets are probably nearing or even past peak production. 147 MMcf/d makes up less than a fifth of the required gas to feed Train 1. If Pieridae extracts 243 MMcf/d continuously, which is impossible given the necessary decline in production, it would dry up its reserves in less than 14 years. To add to the problem, they would not even produce a third of the gas required for Train 1.

The numbers are consistent with Pieridae’s business model, which relies on outsourcing at least 50% of its gas, as outlined in a Laurentian bank document: « To supply both LNG Trains will require up to 1.5 bcf/d of raw gas, and Pieridae will likely seek to own up to 50% of that requirement, and source the remainder through the North American gas grid. Our section on Transportation [Exhibit 1] identifies the pipeline routes available to the Goldboro facility. »

So far, Pieridae managed to acquire only 1,078 bcf of conventional natural gas reserves. It is highly unlikely they will be able to feed Train 1 entirely with conventional gas from Alberta, since the entire Western Canada conventional gas supply is slowly drying up as well.

Conventional production declines in Alberta and British Columbia

The light green portion of the graph (Exhibit 4) represents conventional natural gas production in Western Canada from 2000 to 2040, with a clear trend towards exhaustion.

In its Canada’s Energy Future 2018 Supplement, the National Energy Board of Canada states: “Western Canada conventional gas is projected to decrease from 2.96 bcf/d in 2017 to 0.87 bcf/d in 2040.” This decline rate is more than threefold. If it is applied to Pieridae’s assets, we could forecast its conventional gas production would decrease from 243 MMcf/d to 71 MMcf/d, with an average of 157 MMcf/d. These estimations are very close to what Pieridae holds as reserves, spread over the same time span.

Western Canada Solution Gas (shown in yellow) “is gas produced from oil wells in conjunction with the crude oil.” Heavy oil does not contain any natural gas or lighter solvent, hence the term “heavy”. Solution gas comes from light oil. A large amount of light oil currently extracted in Western Canada comes from fracking, and the only way to increase solution gas supply is to exploit more fracked oil in Western Canada. This scenario would not allow Pieridae to sell it to Germany as conventional gas.

Pieridae already processing fracked gas at not-yet-acquired Caroline plant

The deal between Pieridae and Shell involves the transfer of three gas processing plants, including a more recent facility, the Caroline plant. In its latest annual financial statement, Pieridae declares the following: “The Company also generates gas processing revenue of $6.8 million (December 31, 2018 $0) for fees charged to third parties for processing through facilities in which Pieridae has an ownership interest.” The facility is most likely processing gas for Shell as part of the deal to acquire its acid gas assets. The article Sweet future for Shell’s Caroline Plant confirms the Caroline field is nearing 95% recovery and that Shell wanted to convert the Caroline plant to process gas from the Rocky Mountain House play. On its corporate website, Shell states it “has been pursuing the production of light tight oil, gas and liquids from the Duvernay play, in this area.” Duvernay is a tight play known to require fracking for oil and gas extraction.

Consequently, Pieridae will have the opportunity to buy fracked gas already processed at the Caroline plant. If Pieridae lacks the reserves to feed its first train with conventional gas only, will it buy the gas from its partner Shell? Or will it find another partner who could provide more expensive, but already treated fracked gas? Alfred Sorensen partially answers this question in the April 16, 2020 corporate presentation: “The most significant asset we acquired was three deep cut plants: the Jumping pound, Caroline and Waterton. Between the three of them, they represent about 750 million a day of processing capability, and that number is a big part of how we’re going to supply our first train. One train requires about 800 MMcf/d, so you can see the two numbers are very close in relationship. […] That’s how […] we will begin to service our first train.” In the same presentation, we learn that Pieridae produces 204 MMcf/d, but processes 420 MMcf/d of gas at the three plants it will soon own. The difference is most likely fracked gas.

Pieridae has a deal with Shell to process its gas from the Rocky Mountain House play. They want to use all the processed gas at the three plants to feed the first train of the terminal, which will supply Uniper.

One way or the other, it appears impossible for Pieridae to feed its first train entirely with conventional gas from Western Canada. Nowhere will they find the 800 MMcf/d of conventional natural gas required to feed the terminal’s first train over the next twenty years.

Could Pieridae rely on assets in Eastern Canada and the U.S. to find the missing part of its conventional natural gas?

Conventional gas in Eastern Canada?

Pieridae uses the map (Exhibit 1) during many corporate presentations to indicate where it will source its gas from and how it will be transported all the way to its terminal. Let’s look at these sources, beginning at the furthest east gas deposit.

Nova Scotia’s Sable field : gone!

“The third option for Pieridae is to source gas from offshore Nova Scotia. While the existing Sable Island and Deep Panuke gas fields are being decommissioned, the existing 300 MMcf/d production platform and Sable pipeline direct to Goldboro provide significant advantages.” (Excerpt from “On Track to Become Canada’s First Major LNG Exporter”, January 2018) In a January 3, 2019 press release, the Nova Scotia government stated: “A few days ago, one chapter of Nova Scotia’s offshore story came to an end when the Sable Offshore Energy Project delivered the last of its gas to our province.” This apparent source of gas for Pieridae’s executive is in fact so depleted that Nova Scotia’s government says it “delivered the last of its gas.”

New Brunswick : A moratorium on fracking after traumatic events

In 2014, New Brunswick introduced a moratorium on hydraulic fracturing. Before this historic moment, dozens of groups from across the province united against the industry. One of them, the New Brunswick Anti-Shale Gas Alliance, went on to sue the province. After the pro-shale Conservatives’ electoral loss and the subsequent implementation of the moratorium, the lawsuit was dropped. However, the Alliance remains active and diligent: it has stated it will go back to court if any exemption is approved.

In the years prior to the moratorium, Indigenous opposition escalated from demonstrations to civil disobedience, culminating with a militarized RCMP raid on a protest encampment. Arrests were made, and police cars were burned (Exhibit 5) – a traumatic incident that still affects Indigenous and police relationships six years later. An investigation of the RCMP’s misconduct has been completed, but not yet released.

The moratorium targets hydraulic fracturing, not drilling for gas. Since all New Brunswick gas reserves require fracking, no drilling is conducted in the province. And those reserves include Pieridae’s gas leases.

Five conditions must be met to lift the moratorium: a social license, a regulatory regime able to enforce health and environment protection laws, a plan to mitigate impacts on public infrastructure and manage wastewater, meaningful consultations with First Nations, and a royalty structure benefitting New Brunswick residents.

Pieridae threatens the New-Brunswick moratorium on fracking

Pieridae has corporate interests in New-Brunswick assets (Exhibit 6) that could easily be connected to the Maritimes and Northeast pipeline (M&NE, dark blue line in Exhibit 1). During its presentation to shareholders in June 2018, Pieridae stated that “if Conservatives are elected, they have indicated they will lift the fracking moratorium.”

A year after their election, the Conservatives attempted a partial exemption to the moratorium in the Sussex area, where mayor Marc Thorne wishes the industry would resume its activities.

The McCully Field, currently the only area being considered for moratorium exemption, is represented in the lower left corner of the map (Exhibit 6) as two plots shaded in light green and gray, around the towns of Sussex and Sussex Corner. As the legend shows, Pieridae leases—in red—lay far to the east.

In the areas around Pieridae’s leases, citizens strongly oppose the shale gas industry. In fact, multiple municipalities such as Hillsborough, Memramcook and Alma have passed local ordinances against shale gas, and the provincial government gave its word to comply. The major city of Moncton, which gets its water from the leased area, has also passed an ordinance against the shale gas industry. Opposition is strong among the Wolastoq and Mi’kmaq Indigenous peoples in the province.

For now, the demand for gas in New Brunswick is low. Provincial needs are met by neighbouring fracked gas fields in the Northeastern United States. A new LNG export terminal in the province next door would increase pressure to lift the fracking moratorium in New Brunswick, against the will of the local Indigenous people and population. Pieridae might not use the German loan to directly develop its claims in New Brunswick; however, the company most likely has the will to exploit these claims once Train 2 is completed. The Goldboro LNG project and Pieridae’s plans will create a push to lift the moratorium as soon as it’s time to start drilling the area. The situation seems similar in the neighboring province of Quebec.

Pieridae’s assets in Quebec : small unconventional reserves

The Quebec connector pipeline (Exhibit 1) does not yet exist, since the resources are still untouched. The pipeline would connect the Gaspé peninsula (see map in Exhibit 7) to the existing M&NE Canada system. Pieridae abandoned most of the fields shown on the map in 2019 and only owns the Matapedia, Bourque and Gaspé fields at this time.

Pieridae owns three wells in the Bourque area. In a presentation to shareholders from June 2018, the company outlines that “initial production from Quebec resources will come from the Bourque field in the Gaspé peninsula” and that “permitting work for fracking [is] to be done in 2019.” The 144 bcf of prospective natural gas resources in the Bourque field (see the Sproule report, Table 6) would only provide around 1 to 3% of the gas needed for both Goldboro terminal trains over the 20-year contract with Uniper. According to the report: “The Forillon Reservoir is estimated to be in the 0.01-0.02 mD permeability range. Analogous reservoirs of this permeability range have been successfully developed using HMSF [Hydraulic Multi-Stage Fracturing] technology, however, most of these analogous reservoirs are in tight sandstone and shale reservoirs.”

No well has been drilled in the Matapedia field. Furthermore, two of the three existing Haldimand wells will need to be closed due to a Quebec regulation that prohibits exploration closer than a kilometer from residential areas.

All the gas Pieridae could send the Goldboro terminal from the Gaspé peninsula would be fracked gas. Unfortunately for the company, social licences for fracking in Quebec do not exist. After a year-long protest camp blocking the Galt project (which belongs to another company and is close to being developed), a survey was conducted in the fall of 2017. This survey revealed only 25.6% of the local population supported the Bourque project if fracking was needed. The surveyor did not mention the company’s independent report, according to which the Bourque site cannot be developed without fracking. Closer to home, in Haldimand, only 12.4% of the local population supports oil and gas development if fracking is required, which is the case. The majority of residents (49.3%) would oppose Pieridae’s project even if no fracking were done.

Pieridae’s intent to feed its terminal with gas from the Gaspe peninsula would put pressure to develop an area barely touched by fracking.

Marcellus and Utica regions : Mostly fracked gas

In 2014, conventional extraction of fossil gas in the Marcellus region declined to 5% of the total extraction volume, i.e. about 750 MMcf/d for the whole play. In the Utica region, conventional fossil gas production gravitated around 180 MMcf/d for over 5 years before the shale boom in 2012 and 2013.

Unless Pieridae signs agreements to buy conventional gas from the Utica and Marcellus plays, 85% to 95% of its purchases will consist of fracked gas. This proportion is very likely to increase in the next 20 years, as the conventional supply will eventually dry out. A long-term agreement is just speculation, since Pieridae only plans to use gas resources south of the U.S. border as a backup if Eastern and Western Canada reserves are not enough to feed its terminal.

Germany’s KfW loan guarantee : Lack of conventional reserves and pressure to develop fracked gas in Eastern Canada

Here are the words of Stéphanie Fortin, spokesperson for GNL Québec, a similar sized LNG project in Saguenay, Quebec : « Nous avons toujours été clairs et transparents concernant la provenance et la méthode d’extraction du gaz naturel qui serait utilisé dans le cadre de notre projet ; 85 % de notre approvisionnement sera effectivement extrait selon la méthode de fracturation hydraulique. » (“We have always been transparent on how we will source and extract the natural gas used for our project; 85% of our supply will actually be extracted through hydraulic fracturing.”) GNL Québec and Goldboro are similar projects with similar sources, except that GNL Québec does not hold a permit to import U.S. gas and then export it. Therefore, it cannot rely on fracked gas from Utica or Marcellus shale south of the U.S. border. GNL Québec also will not tap into Quebec or New-Brunswick’s risky fracked gas assets. All the gas would come from Western Canada, and the company’s spokesperson clearly states the mix contains no more than 15% conventional gas. In the future, this proportion will only decline.

Despite Pieridae’s efforts to produce its own gas and buy upstream assets, it must face the reality that conventional fields are depleted. The company must admit it cannot provide 800 MMcf/d of conventional gas to the Goldboro terminal, even if this means losing the US $4.5 billion loan guarantee from KfW to build the first train and expand upstream assets.

Does Pieridae know about the current decline in conventional gas production and resulting price hikes? When they applied for a licence to import and export before the National Energy Board of Canada, they produced a study by Ziff Energy, a division of Solomon Associates. Here is what Ziff Energy had to say about conventional gas in North America:

« 6.2.2.4 Conventional Gas

Gas from reservoirs with greater permeability has been developed since the late 19th century. Most conventional-gas plays are mature, higher cost, and have passed their peak production. Reserves per well are small, resulting in high costs. Before the advent of shale gas, a record level of drilling activity was required to maintain gas production levels in North America. Aggregate gas production has been in decline for more than a decade. For example, the US Gulf of Mexico region, the former workhorse of North American gas production, is declining mainly due to the sharp fall in gas production on the shallow-water Gulf of Mexico shelf. Some old, mature plays are experiencing a new lease on life as producers apply new and evolving technologies, sometimes with spectacular results, such as the Granite Wash in the US Anadarko basin. Ziff Energy assumes the production declines will continue, though at a moderated pace as improved technologies (horizontal wells, multistage fractures) enhance play economics. »

This explanation comes from Pieridae’s own expert report. Of course, the US $4.5 billion loan guarantee from the German government is a good enough reason to lie about the acquisition of Ikkuma and Shell’s “conventional” assets. The Goldboro LNG terminal would not only rely on tight and shale gas supply, but also also increase the demand for fracked gas in Eastern Canada. This would put pressure to lift the ban on fracking in New Brunswick and push against social license requirements, as well as a partial ban, in Quebec. For this reason, Germany must not commit to a loan guarantee for the Goldboro LNG terminal project.